Blockchain technology has been revolutionizing the computing industries for almost a decade. For the last few years, blockchain based industries especially cryptocurrencies have seen a lot of evolution over the course of time. And along each step, the value and fame of each blockchain product has exponentially increased.

This amazing technology is the came into limelight back in early 2010s, as Bitcoins took the world over like a storm. However,for most individuals and established platforms Blockchain is still a complicated interpretation: Blockchain is a distributed, decentralized digital public ledger. But allow me to break this down into simpler words.

What is Blockchain Technology?

As the name suggests, blockchain is, practically, a chain of blocks connected with each other through some data structure. It’s a public digital database shared through a vast computer network. All systems that are linked to the blockchain network are called nodes. Identical copies of each transaction are documented on all blockchain nodes. Therefore, in order to manipulate any record, changes are necessary to each node.

Blocks, in the above particular instance, refer to digital data of all transactions in the network. That includes the schedule, the period of time and the transaction stakeholders. Whenever a new transaction is started a new block will be registered. This new block is then linked to the existing previous block, and therefore the name, blockchain.

With all these explanations, let me rephrase the concept of Blockchain technology for you.

Blockchain is an incorruptible digital economic transaction ledger that can be used to record all of the value.

What is Blockchain ledger

A blockchain is a distributed ledger that is completely open to any and everyone on the network. Once an information is stored on a blockchain, it is extremely difficult to change or alter it. Each transaction on a blockchain is secured with a digital signature that proves its authenticity. Due to the use of encryption and digital signatures, the data stored on the blockchain is tamper-proof and cannot be changed.

Blockchain technology allows all the network participants to reach an agreement, commonly known as consensus. All the data stored on a blockchain is recorded digitally and has a common history which is available for all the network participants.

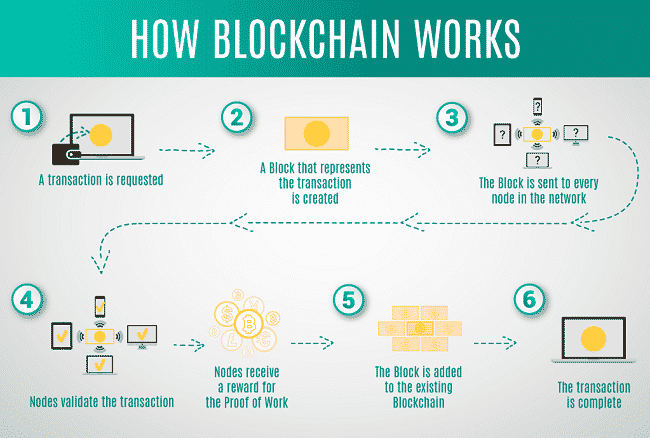

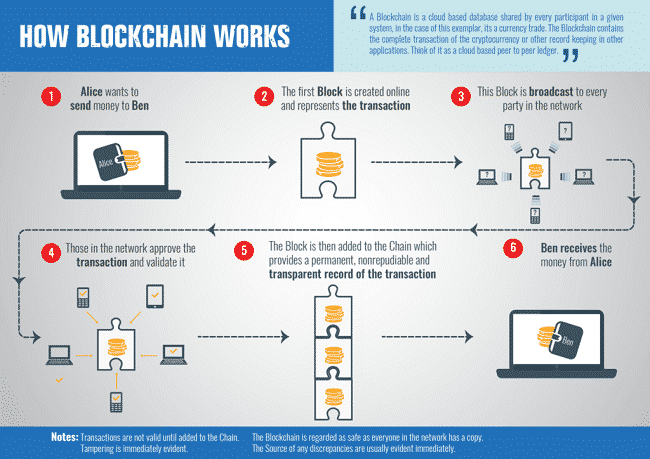

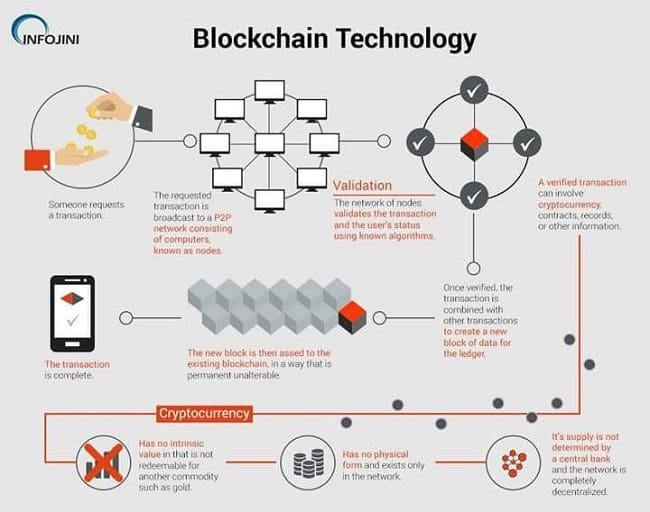

How does Blockchain Ledger Work?

But how does a decentralized digital blockchain ledger really work?

When attempting to explain blockchain, people are often sidetracked in technical sophistication, but the fundamental concept is universal and straightforward. We have factual information that we do not want someone else to unlock, duplicate or manipulate, but there is always a likelihood that it may be hacked or compromised on the internet. Blockchain gives us a consistent foundation we know won’t affect once we put anything on it and only verify a transaction if it meets the criteria.

Blockchain data is actually distributed among all users so that every user has his own copy of block hashes. If there’s a new transaction, its information is spread out over the entire network. A new block of transactions is added to the chain once it has been validated. Every user on the network then updates his copy of the blockchain information. This is how the blockchain ledger becomes public and eliminates external bodies.

Moreover, since every block contains the hash of previous block, it is impossible to alter just a single block without changing the entire chain completely. For instance, if a hacker alters information in Hash#1, the stored information of Hash#1 in Hash#2 will also change which will in turn alter Hash#2 and so on.

Whole blockchain would be identified as corrupt right away and the user would report the attack. This makes blockchain ledger an unchangeable (and thus a highly secure) technology.

The high security of blockchain technology and its decentralized nature are in fact the main reasons behind its numerous applications. The blocks of a blockchain act as secure containers that can contain any sort of information. This is why blockchain is being employed in all sorts of areas like education, healthcare, trade industries etc. to ensure higher security at faster work rates.

Types of Blockchain

There are primarily two types of blockchains; Private and Public blockchain. Before we get into details, let us first learn what similarities do both of theseblockchains share. Every blockchain consists of a cluster of nodes functioning on a peer-to-peer (P2P) network system. Every node in a network has a copy of the shared ledger which gets updated timely. Each node can verify transactions, initiate or receive transactions and create blocks.

Public Blockchain

A public blockchain is a distributed ledger system that is non-restrictive, with no permissions. Anyone who has internet access can sign in to become an authorized node on a blockchain platform and become a part of the blockchain network. A node or user that is part of the public blockchain is authorized to access current and past records, verify transactions, or prove work for an incoming block, and undertake mining activities. The most basic use of public blockchains is to cryptocurrencies mining and exchange. Thus, the Bitcoin and Litecoin blockchains are the most common public blockchains.

Private Blockchain

A private blockchain is a blockchain operating with restrictions or permissions only in a closed network. Private blockchains are usually used within an organization or enterprise where participants of a blockchain network are only select members. The level of security, permissions, permissions, accessibility is in the control organization’s hands. Private blockchains are therefore similar in use as a public blockchain but have a small, restrictive network in place. Private blockchain networks are deployed for voting, management of the supply chain, digital identity, property ownership etc.

Evolution of Blockchain

In the past decade, Blockchain has been a subject to a lot of development. From the initial proof-of-concept in Bitcoin to modern proof-of-stake of Cardano, Blockchain has taken major developmental steps along the course of time.

First Generation of Blockchain – Bitcoin

The first blockchain was conceptualized in 2008 by an anonymous group, Satoshi Nakamoto. The concept and technicalities are described in an accessible white paper, Bitcoin, a peer-to-peer electronic cash system. These ideas were then first implemented in 2009 as a core component supporting Bitcoin, where it served as the public ledger for all transactions.

The invention of the blockchain for the Bitcoin made it the first digital currency to solve the double spending problem without the need of a trusted authority or central server. It was only later, that we came to really separate the concept of the blockchain from that of its specific implementation as a currency in Bitcoin.

We came to see that the underlining technology had a more general application beyond digital currency in its capacity to function as a distributed ledger tracking and recording the exchange of any forms of value.

Second Generation of the Blockchain – Ethereum and Smart Contract

Within just a few years, the second Generation of Blockchain emerged, designed as a network on which developers could build applications. Essentially, the beginning of its evolution into a distributed virtual computer. This was made possible by the development of the Ethereum platform.

Ethereum is an open-source public blockchain based distributed computer platform featuring smart contract functionality. It provided a decentralized Turing-complete virtual machine which can execute computer programs using ta global network of nodes.

Ethereum was initially described in a white paper in late 2013 with a goal of building distributed applications. The system went live almost two years later and has been very successful attracting a large and dedicated community of developers, supporters and enterprises.

Third Generation of Blockchain – Blockchain 3.0

Blockchain, over the course of time, has seen a lot of constraints in scalability and mining expenses its networking system. In response to these constraints, a third generation of blockchain networks are currently under development. Many different organizations are currently working on building this next-generation blockchain infrastructure.

Such projects include Dfinity, NEO, EOS, IOTA and Ethereum itself. Currently, Cardano and IOTA are both considered to be the third generations of blockchain and the future of the industry.

Why do We Need Blockchain Technology?

You can request transaction from someone you’ve never met on a trustless channel like a blockchain, and once the payment arrives, the system will make sure that the transaction is legitimate and verified, within a matter of moments. Existing technologies like the SWIFT banking network currently take 2-3 days to do just that.

In addition to efficiency, automated processes offer reduced cost. Many of the cost of traditional banking operations and transactions are reduced with blockchain. This is made possible by the elimination of many of the cost-intensive banking processes. The saved cost can be redirected to other equally important purposes.

Another concern blockchain technologies fix is the major issue of dual-spending. The issue of dual-spending centers round the assumption that somebody can make an entry on a database and then go back and rewrite it if they have the authority or power to do so. Fundamentally, that would authorize someone to spend the very same money twice.

Blockchain technology is permanently evolving. In order to bring forward unique innovations, governments and enterprises alike are rapidly investing in blockchain. It is becoming increasingly clear that the Blockchain technology is here to stay and thrive, and anyone who doesn’t understand it would soon be left behind.